Guide to Key Person Protection

This is our fourth post on Business Protection, helping you to understand if you need Business Protection Assurance, and if so, what parts of it apply to you. You can also read our Introduction to Business Protection, guide to Shareholder (or Partnership) Protection, and Guide to Business Loan Protection.

This is our fourth post on Business Protection, helping you to understand if you need Business Protection Assurance, and if so, what parts of it apply to you. You can also read our Introduction to Business Protection, guide to Shareholder (or Partnership) Protection, and Guide to Business Loan Protection.

Key Person Protection at a glance:

| Definition | Who is covered? | Who benefits? |

| Life assurance purchased by a business, designed to pay out if a key member of staff dies or suffers a critical illness. | Any key member of staff, e.g. chief executive, finance director, salespeople, director or owner. | Policy proceeds would be paid directly to the business, giving it a vital cash injection to help recruit a suitable replacement, or mitigate lost profits. |

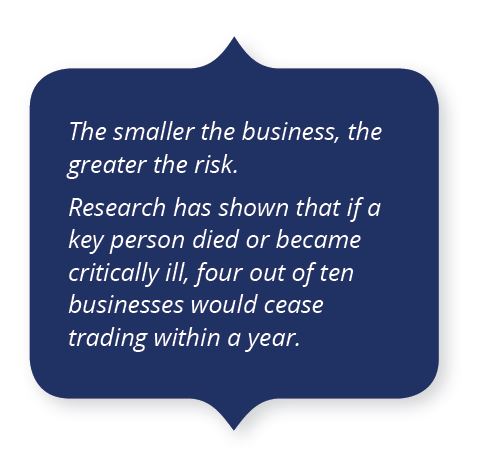

Insuring your business’ key individuals is arguably just as important as the more obvious cover for the trading premises, fixtures and fittings. Vulnerability can occur where a vital employee becomes critically ill, or dies.

The absence of any key person can cause problems. As well as losing their knowledge and experience, you may find that it affects creditors’ and lenders’ attitudes, resulting in cash-flow problems, or affects relationships with your key clients. You may have to rethink or even abandon plans for the company’s future.

The first step is to identify those individuals who are essential to the success of your firm. If you think that their loss would have a significant financial impact, then Key Person Protection can provide a cash injection to the business while a replacement is found, or while the individual recovers.

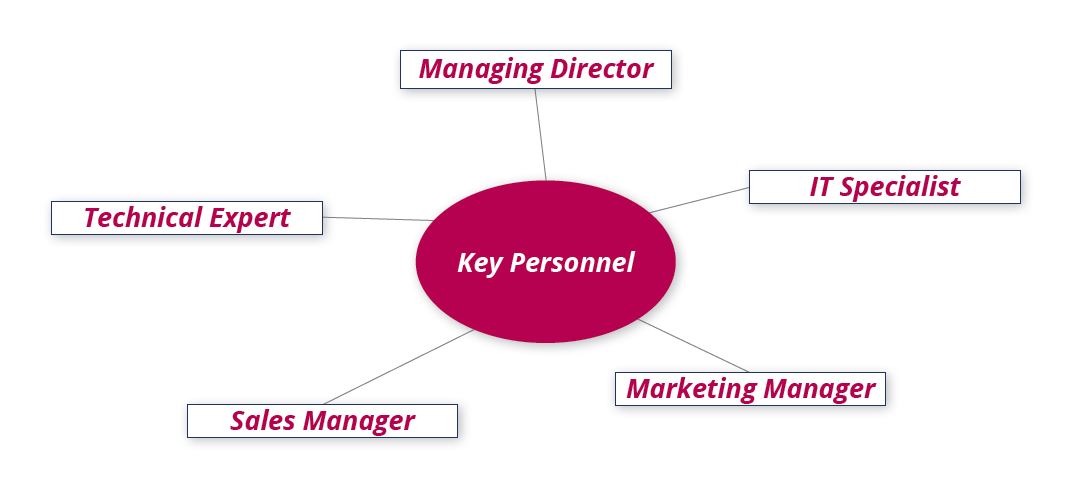

Who is a key person?

Virtually anyone could be a key person, but the positions that are typically seen as key to a business are:

How is cover calculated?

Typically, cover will be arranged around the cost of replacing the individual based on a multiple of their earnings. For example, 10 x salary for life cover, with a lower figure (5 x salary) for Critical Illness cover.

Another method is to look at replacing the profits that the key person is responsible for. As a guide, cover may be arranged for, say, twice the gross annual profit they generate or five times the net profits attributable to that person.

Taxation of Key Person policies

It may be possible to offset the cost of Key Person Protection assurance against your Corporation Tax bill, as it is often treated as an allowable business expense.

If the premiums have been offset against profits, any payout from the policy will form part of the company’s revenue (trading receipts) for that year, which may increase your overall Corporate Tax bill.

In order to offset the cost of this insurance against tax, certain criteria conditions have to be met:

- The policy is a short-term assurance. HMRC does not stipulate a length of time, but takes into account how long the employee will be of benefit to the business. The policy should not be for ‘whole of life’, or extend beyond the employee’s contract of employment.

- The policy is intended to cover loss of profits.

- The relationship is between employer and employee. Owners and controlling directors can be covered, although they are unlikely to receive tax relief on the premiums as HMRC may argue that the policy proceeds are primarily for the benefit of the person covered, because they own a majority of the shares.

Next up, Relevant Life Policies.

Please note, this article is for information only and does not constitute specific advice. We recommend you talk to a qualified professional before purchasing Business Protection Assurance.

By Craig Hilton DipPFS

By Craig Hilton DipPFS

Associate Director

Gibbs Denley

Email Craig